Home: ForBestAdvice - People - Bob

Brinker - Bob Brinker's Stock Market Outlook and Current Marketimer Portfolio Advice

Home: ForBestAdvice - People - Bob

Brinker - Bob Brinker's Stock Market Outlook and Current Marketimer Portfolio Advice

|

Moneytalk Show Review Bob Brinker's Stock Market Advice and Answers to Model Portfolio Questions July 21, 2013 |

|

|

|

||

| July 21, 2013 Newsletter Excerpts - Editorial

Comment ("EC") by David Korn: Bob Brinker Fan Club Home Page - Bob Brinker's Asset Allocation History |

||

|

David

Korn's Stock Market Commentary,

Interpretation of Moneytalk (Bob Brinker

Host), Financial Education, Helpful Links,

Guest Editorials, and Special Alert E-Mail

Service. Copyright David Korn, L.L.C.

2013

DAVID

KORN'S

COMMENTARY: Excerpts

below

|

|

|

MARKET NUMBERS AS OF FRIDAY JULY 19, 2013Current Series I Bond Rates BOB BRINKER’S CURRENT STOCK MARKET ADVICE Brinker Comment: The S&P 500 is the benchmark index in the United States as of Friday closed at 1692 represents the all-time historic closing high. EC (David Korn): That was the only direct comment Bob made about the stock market this weekend. Bob remains fully invested. He didn¹t give any indication today that he has an imminent sell issue planned. Kirk Here: Carefully notice Brinker could not pat himself on the back for pointing out a buying opportunity when the market was 20% lower last year because he missed it. The S&P500 is up 18% since last year at 1,433.19 when we reported in our Oct. 10, 2012 summary that Brinker advised "dollar cost average during market weakness." There really hasn't been any weakness (a correction of 10% or more) so I guess people who followed that advice missed out. Maybe he's getting too old but I remember he used to have many buy the dips opportunities in the 1990s before he correctly lowered his allocation to equities (but did not sell all) in January 2000. For more, see Kirk Here: Bob Brinker remains fully invested and has recommended dollar cost averaging in new money into the stock market. Bob Brinker has had his model portfolios FULLY INVESTED, 100% in equities, since March 2003. Bob Brinker's "Marketimer" newsletter missed the biggest bear market since the Great Depression where he was wildly bullish near the top so take his ability to time the stock markets with a grain of salt. For more on this, read "Bob Brinker's Mid 1400's Buying Opportunity." |

LUMP SUM V. ANNUITY Caller: This caller said over the years he has heard Bob generally favor taking a lump sum instead of an annuity payment so you can manage the money yourself. What about if a couple were offered a 5.9% guaranteed rate of return backed by the PBGC for as long as the husband and wife would live. Bob said if you can get 5.9% and it is indexed to inflation in this kind of rate environment, that would be something he would definitely consider especially if it didn¹t have an impact on net worth (such as you didn't need money when you died to leave to someone like a child). Bob noted that having it indexed to inflation was a huge deal because if it was not and you took the lump sum and managed the money yourself, you could take advantage of higher rates if they come down the road. EC (David Korn): Morningstar has a good article in the form of an an interview entitled, "Pension Lump Sum or Annuity: 5 Swing Factors" at the following url: http://tinyurl.com/k9dscbj FLOATING RATE FUND Caller: This caller asked what the risks are in owning a floating rate fund such as the one Bob recommends. Bob said the floating rate income fund he recommends has an extremely short duration of just 4.8 months. It also has a generous yield relative to what is out there in this low yield environment. Bob said when you recommend such a fund, you have to consider your economic outlook. Bob said he is not expecting a recession. Instead, he expects the economy to gradually grow and in that environment he is comfortable with the holdings in that fund. EC: Bob is recommending the Fidelity Floating Rate High Income fund (FFRHX) on the income side in two of his model portfolios. Learn more about floating rate bonds at this url: http://tinyurl.com/lpr4c5z Kirk Here: I wrote an article about Bob's advice in this fund for the blog. See: TAX EFFICIENT INVESTING

Caller: This caller has the majority of his money with Vanguard. In August

2009, he took advantage of an offer by Vanguard to design a financial

plan for him. At the time, he had a portfolio that consisted of

50% stock funds and 50% cash. The stock funds are held in a

tax-deferred account and the cash is held in a taxable account.

The plan he choose was a consolidated portfolio which consisted of 60%

stocks, 40% bonds, but they wanted him to sell 80% of his stock funds

and buy the total bond market and then with the cash reserves in the

non-sheltered account, they wanted him to buy stock funds (83% total

stock market index and 17% international index). He didn¹t do it

and wanted to see if Bob agreed because they were still recommending

it.

Bob agreed with the caller and said it didn¹t sound like it made good sense from a tax strategy perspective. Bob said we have been in a rising market since 2009 and so there would be taxes on capital gains and in addition to that, the total stock market index produced about 2% annual return in dividends. You would have to pay taxes on those and given how low bond rates are, why would someone want to put their stock funds into a taxable account and put the bond funds that have historically low yields in a tax-privileged account? Bob said he didn¹t think that sounded like a good idea to him.

Kirk Here: I don't

think Bob was paying attention to what the caller was asking or he

doesn't understand taxes! There would be no taxes to pay by

selling the stocks in the IRA. The caller would be able to harvest the lower capital gains rates

on appreciated bond funds in his taxable account then use the money to

buy more more tax efficient index funds with the taxable money.

Any gains on equities plus the dividends in the taxable account would

then be taxed at the favorable capital gains and dividend rates. These

are all lower than taking the gains out of IRAs as ordinary income. Then

with the cash raised from selling stocks in his IRA, he would buy

bonds. Remember that ALL distributions from IRAs are taxed as

ordinary income. You lose the tax advantage of dividends and

capital gains on stocks held in IRAs!

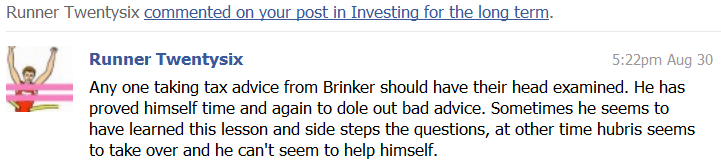

Kirk Here: If you still believe Brinker over me, then here is a good article entitled, "The importance of Tax-Efficient Investing" from the Schwab Center for Financial Research. It is written by Rande Spiegelman who used to help me answer questions for the "Bob Brinker Fan Club" discussion forum back in the late 1990s and early 2000s while he worked at KPMG and they allowed him to post on internet message boards. BTW, these days I have a public discussion forum on Facebook called "Investing for the Long Term" that you are welcome to join. Update Aug. 30, 2013: Here is a Facebook comment on this article from a member after I asked for comments on this article.  VTI - Vanguard Total Stock Market ETF

Top of page

Kirk Here: My core and explore

portfolios recently made all time highs!!!

For more conservative investors who have no interest in individual

stocks, I co-edit "The Retirement Advisor" where our most aggressive

model portfolio is slightly less aggressive then the "core conservative

portfolio" in Kirk Lindstrom's Investment Letter." For more

explanation, see "Kirk's Two Investment Letters - Which is Best for You?

Subscribe

NOW Ask about a FREE ISSUE if you Subscribe Today!

Article:

How

to

Get the Best CD Rates(Your 1 year, 12 issue subscription will start with next month's issue.) David and I are very proud of our performance for

"The

Retirement Advisor:"

David's Newsletter: If you would like a free sample of David's complete Newsletter and our "Retirement Advisor" newsletter, then click this link to send an email request and please tell us a bit about yourself too. Return to: Bob Brinker Fan Club Home Page - Top of Page If you want updates

on what Brinker is saying on Moneytalk delivered

to your email box, often within 24 hours after

Sunday's show, then send us a note at TalkAboutMoney@gmail.com

and ask to get on our mailing list.

|

|

|||

|

(More Info, Testimonials & Portfolio Returns)

ForBestAdvice.com:

Your place for information and advice about anything

and everything |

|||

|

|

bbfc

sitemeter |

To

advertise

on this page, please contact advertising@<REMOVE>forbestadvice.com |

|