Home: ForBestAdvice - People - Bob

Brinker - Bob Brinker's GNMA Advice from March 18, 2012

Moneytalk Show

Home: ForBestAdvice - People - Bob

Brinker - Bob Brinker's GNMA Advice from March 18, 2012

Moneytalk Show

|

Moneytalk Show Review Bob Brinker's Stock Market Update for 2012 March 18, 2012 |

|

|

|

||

| March

18, 2012 Newsletter Excerpts - Editorial

Comment ("EC") by David Korn: Bob Brinker Fan Club Home Page - Bob Brinker's Asset Allocation History |

||

|

|

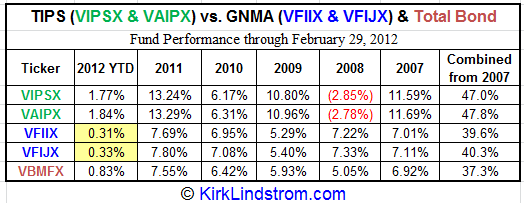

GNMA Advice - Continues to recommend GNMAs Caller: This caller asked Bob what she should do with her GNMA fund given that rates have gone down and if she sells, what should she go into? Bob said the second part of the question was the hard part and a problem. Bob said he likes to invest for income in the context of an overall portfolio. If you follow Bob’s lead, you are either going to go with his Income Only portfolio or a Balanced Portfolio which has 50% in fixed income. Kirk Here: Bob Brinker's Marketimer Model portfolio's One and Two are 100% in equity mutual funds and have been 100% in equities since March 2003. When the S&P500 was at 1565 several years ago, his "balanced" Model Portfolio #3 was two thirds in equities with only a third in fixed income which included (and still does) Vanguard's GNMA fund with ticker symbol VFIIX. (VFIIX quotes and charts) Bob said he has GNMA component in both of those portfolios and continues to hold them. Bob said he would rather that be a given percentage of a portfolio, but not the entire portfolio. Bob said in his Income Portfolio, GNMA is one of five holdings and in the Balanced Portfolio there are other holdings as well. Kirk Here: Bob Brinker used to call his "Income Portfolio" his "Fixed Income Portfolio" but after the market nearly doubled from the 666 in 2009 to 1258, In January 2011, Brinker added a mutual fund that has a mixture of stocks and bonds (Vanguard Wellesley Income Fund - VWINX) to his "Fixed Income Portfolio." Some of us "critics" pointed out in blogs that this was no longer "fixed income" so he changed the name of the portfolio over the next two months. In his Feb. 2011 Marketimer he changed the name in the text and in March 2011 issue he changed the name on the table listing what is in the portfolio. We took great "pride" in "assisting" Brinker more accurately represent his portfolios! |

|

Caller: This caller heard some talk shows over the weekend and he heard a lot of concern over the GNMA Fund because of inflation fears. Bob said the people who are voicing that concern probably never recommended them in the first place. GNMA has been one of the best performing fixed income securities for a long time, even through a difficult time. Kirk Here: GNMAs have done very well, better than equities for the last five years! The TIPS funds, that David and I recommend in our Retirement Advisor newsletter, have done even better! The S&P500 is "only" up 7.2% over this same period. You would think that the "world's most trusted financial advisor" who advertises himself as a "Market Timer" would have dumped equities from his portfolios and gone to GNMAs (or TIPS) if he could really time the markets.  Kirk Continued: I prefer index funds for "core portfolios" but I have traded Vanguard's GNMA fund in my newsletter "Explore Portfolio" on and off since buying in 1999 with profits I took in some of my technology stocks. I sold the last of my GNMA funds on Sept. 18, 2009 and then bought TIPS a few weeks later. As the table above shows, it was pretty good timing, if I say so myself! Bob said the Vanguard GNMA Fund is trading within 1-2% of its all time high. At the same time, you will have fluctuation in net asset value and so if you are unwilling to accept that fluctuation you can set a mental stop, but then you might sell and have cash and not have many places to put it in this low interest rate environment. Kirk Here: Don't be fooled by all this "happy talk" about how well fixed income has done over the past five years. Bob Brinker's 5-year returns between 1/1/20007 through 12/31/11 were 4%, 6% and 14% for his model portfolios one, two and three, respectively. Only his "balanced" model portfolio three reached double digits for total return over five years (not counting the cost of the Marketimer). The "balanced" model portfolio #1 that David and I recommended beat Brinker's balanced portfolio by doing 19.5%. Our less risky portfolios returned 24% and 31% (see below). EC (David Korn): Here is a link to an article entitled, “What to do about low interest rates” that includes a reference to holding a GNMA Fund: http://tinyurl.com/84n86yw Kirk Here: My explore portfolio

is off to a great start too up 10.6% YTD as of 3/19/12

with ONLY 2/3rds in equities!!!!

Long

Term Results that Speak for Themselves

Since 9/30/98 inception, "Kirk's Newsletter Explore Portfolio" is UP 390% vs. the S&P500 UP only 51% vs. NASDAQ UP only 57% (All through 12/31/11) Subscribe NOW and get the March 2012 Issue for FREE! ! (Your 1 year, 12 issue subscription will start with next month's issue.) (More Info, Testimonials & Portfolio Returns) Kirk Here: The Fed is trying to create inflation to inflate us out of trouble. CPI inflation is running at 2.9% per year and Core PCE inflation, the Fed's preferred method of measuring inflation, is running just above the Fed's target of 1.8 to 2.0%. This year and last year I bought the maximum $10,000 in Series I Bonds to add to my i-Bond portfolio. Some of my older iBonds have a 3.0% base rate so with the current inflation rate they are paying me a whopping 7.67%! But, even the new ones that "only" pay the rate of inflation are paying 3.06% for the next six month. With CPI running at 2.9%, I expect they will pay more for the next six months. That sure beats US Treasuries even if you sell them and pay the small penalty if you need the cash before the five year penalty period passes. Top of page

Kirk

Here: David and I are very

proud of our performance for "The

Retirement Advisor:" Note how our

"most conservative portfolio, with zero stock

market exposure, made money every year. The

Brinkers can's say that about ANY of their "income

portfolios" in either of their two newsletters.

The Retirement Advisor

Portfolio Performance By Year Through December 31,

2011

CLICK HERE to download a FREE issue of "The Retirement Advisor."

Website for more information and annual Performance Data If you would like a free sample of David's complete Newsletter and his "Retirement Advisor" newsletter, then click this link to send an email request and please tell us a bit about yourself too. Return to: Bob Brinker Fan Club Home Page - Top of Page If you want updates

on what Brinker is saying on Moneytalk delivered

to your email box, often within 24 hours after

Sunday's show, then send us a note at TalkAboutMoney@gmail.com

and ask to get on our mailing list.

|

|

|||

|

|

|||

|

|

bbfc

sitemeter |

To

advertise

on this page, please contact advertising@<REMOVE>forbestadvice.com |

|